“Windfall Tax on UK Banks”

Windfall Tax on UK Banks: What It Means for the Economy, Investors, and You

In recent years, the debate around a windfall tax on UK banks has gained momentum. With rising interest rates, record-breaking profits, and growing public concerns about the cost-of-living crisis, policymakers are considering whether Britain’s banking giants should contribute more in taxes. But what exactly is a windfall tax? How does it affect banks, customers, and the wider economy? And most importantly, what could it mean for your money?

This article dives deep into the subject of the windfall tax on UK banks, providing clarity on its implications, benefits, risks, and global context.

What Is a Windfall Tax?

A windfall tax is a one-off or temporary levy imposed by governments on companies that make unexpectedly high profits, often due to external factors. Unlike regular corporate tax, which applies consistently, a windfall tax targets extraordinary gains.

In the UK, the idea of a windfall tax on banks is driven by the argument that rising interest rates have enabled banks to earn billions from higher loan charges while passing only minimal benefits to savers. For many critics, this profit surge is not due to innovation or efficiency, but rather a favorable economic environment—making it a prime candidate for windfall taxation.

Why Is the UK Considering a Windfall Tax on Banks?

The debate about introducing a windfall tax on UK banks intensified after reports showed British banks enjoying soaring profits in 2023 and 2024. Key reasons include:

- Rising Interest Rates – With the Bank of England increasing rates to curb inflation, banks benefit from wider profit margins on lending.

- Record Profits – Several high-street banks, including Barclays, Lloyds, HSBC, and NatWest, reported multi-billion-pound earnings.

- Public Pressure – Households are struggling with mortgages, energy bills, and inflation, fueling anger over banks pocketing extraordinary profits.

- Political Debate – Opposition parties argue that banks should contribute more to help fund public services and support citizens in crisis.

How Would a Windfall Tax Impact UK Banks?

If a windfall tax is imposed, UK banks could face billions in additional charges. While it may not cripple their balance sheets, the ripple effects could be significant:

- Lower Dividends & Buybacks – Shareholders, including pension funds, may receive smaller payouts.

- Reduced Lending Capacity – Banks may tighten credit conditions, affecting mortgages, business loans, and personal finance.

- Global Competitiveness – Critics argue a windfall tax could make the UK less attractive to financial institutions compared to other financial hubs.

Benefits of a Windfall Tax on Banks

Supporters of the windfall tax on UK banks highlight several potential advantages:

- Revenue for Public Services – Billions could be redirected into healthcare, education, and social support.

- Fairness – Ensuring corporations contribute more during periods of extraordinary profit.

- Relief for Citizens – Funds raised could be used to reduce the burden of the cost-of-living crisis.

Risks of Imposing a Windfall Tax

While appealing politically, a windfall tax on banks carries potential downsides:

- Reduced Investment – Banks may cut back on investment in technology and innovation.

- Higher Borrowing Costs – To offset taxes, banks might raise fees or lending rates.

- Capital Flight – Global banks could shift operations to friendlier tax regimes, weakening London’s status as a financial hub.

Lessons from Other Countries

The UK is not alone in considering a windfall tax on banks. Similar measures have been discussed or implemented in:

- Italy – Introduced a surprise windfall tax on bank profits, sparking market turmoil.

- Spain – Imposed a temporary tax on banks and energy companies to ease public financial pressures.

- Hungary – Used windfall taxes extensively on banks to fund budget deficits.

These global examples highlight both the benefits and risks of such policies, serving as valuable case studies for Britain.

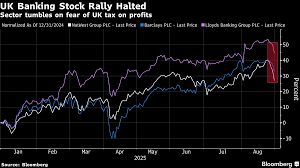

What Does It Mean for Investors and Customers?

If you hold bank stocks or rely on financial institutions, a windfall tax on UK banks could impact you directly:

- Investors: Expect possible dips in share prices, reduced dividends, and market volatility.

- Customers: Mortgage rates, savings interest, and service fees may be influenced depending on how banks react to the levy.

- Economy: A large-scale windfall tax could inject much-needed funds into public spending but may also dampen financial sector growth.

Could the Windfall Tax Be Permanent?

One of the biggest questions is whether a windfall tax on banks would remain temporary or become a long-term fixture. Historically, governments often introduce such taxes as short-term solutions. However, once revenue streams are established, political pressure to maintain them can be strong.

Final Thoughts: Is a Windfall Tax on UK Banks the Right Move?

The idea of a windfall tax on UK banks reflects the tension between public interest and financial stability. On one hand, it offers an opportunity to redistribute unexpected corporate gains to ease the cost-of-living crisis. On the other, it risks discouraging investment, raising borrowing costs, and weakening the UK’s financial standing.

For now, the debate continues. What is clear is that the decision will carry long-lasting consequences for banks, investors, and households alike. As global markets shift and domestic pressures mount, the UK must strike a balance between fairness and financial competitiveness.

✅